by Adedeji Olowe and Khadija Abu

Introduction

Nigerians have increased the amount of money they save over the last 3 years. This, however, has not yet translated into a true savings culture for most Nigerians. Users and providers of financial savings products and services (banks, fintechs etc.) face several challenges which inhibit the ease of providing and accessing tailor-made savings products. Open banking is set to transform the way Nigerians save by creating the opportunity for service providers to access rich customer data and provide innovative savings products and services that are tailored to customer needs..

This article explores the impact of savings on Nigeria’s economy, the issues currently faced by users and service providers, and how Open Banking can address these issues thereby encouraging a better savings culture. This article also contains an interesting and illustrative user journey which demonstrates, step-by-step, how a customer interacts with a consumer savings application to create and automatically fund a savings plan.

Background

The ability for people in a country to save towards their future is one of the key macroeconomic variables in any economy and serves as a crucial pillar of financial inclusion.

The impact of savings on capital accumulation, productivity and economic growth cannot be overemphasized. It provides a way to address emergency needs and kickstart wealth creation while building financial knowledge and skills.

Operating a savings account and being disciplined with savings helps individuals to invest in their future, as well as provide the means to fund emergency needs for cash without depleting other assets, such as personal belongings or business inventory.

It is important to encourage a savings culture, provide relevant savings tools that enable both the banked and unbanked to save. This would improve financial inclusion and economic growth. In addition to helping the economy grow, savings can help individuals reach important goals (such as funding education, asset purchase etc.), create wealth (through investments) and survive difficult times (such as a period of job loss).

The amount of money saved by Nigerians s as a percentage of GDP increased from 15.8% in 2016 to 19.2% in 2018. Some of this growth has been as a result of increased drive from financial service organisations encouraging Nigerians to save and efforts from the federal government through savings initiatives. One of these initiatives was the introduction of the “Federal Government of Nigeria (FGN) Savings Bond” through the Debt Management Office (DMO) to enhance the savings culture among Nigerians while providing an opportunity to contribute to National Development while receiving favourable returns available in the capital market. These initiatives and drive by financial service organisations and the federal government have however not been enough to truly drive a savings culture among Nigerians.

Users and providers of financial savings products and services currently experience challenges that impede the development and maintenance of a true savings culture in Nigeria. Some of these include the cumbersome savings processes and very low rates which do not encourage Nigerians to save. Interest rates on savings in Nigeria vary between 1.25% – 2.5% which is very low and below the country’s inflation rate of about 12.8%.

Furthermore, in the absence of formal savings accounts and tools, the unbanked have resorted to informal methods of saving money, such as keeping cash at home, investing in livestock or jewelry, or saving through informal deposit collectors (“Ajo”, “Esusu”). These informal methods of saving do not always serve the needs of these individuals as they are mostly high risk and unreliable.

Current issues faced by users of Savings products

Low-interest rates – Generally, interest rates encourage savers and low-interest rates discourage savings. The Central Bank of Nigeria has reviewed the minimum interest rates on savings to 1.25%, meaning Nigerian savers will get at least 1.25% interest on their savings per annum.

This is extremely low, especially with the inflation rate at 12.82% as at August 2020, meaning the value of money saved depreciates with time and saving in Nigeria is tantamount to paying banks to keep your money for you. For example, at an interest rate of 1.25% p.a, it will take ~57 years for the amount you save in a bank to double. This does not take into consideration the numerous bank charges like account maintenance fees that will also deplete the amount saved.

Countries with high savings rates like India (interest rate between 3 – 7.5% and inflation rate at 7.6%), Singapore (interest rate between 1.2% – 3.88% and inflation rate at 0.6%) and China (interest rate between 3.85% – 5.77% and inflation rate at 2.9%) have high savings as a percentage of GDP thereby corroborating the theory that high-interest rates encourage individual savings in any country.

Cumbersome and expensive process of saving – The process of saving money automatically for Nigerians can be cumbersome, especially with traditional Nigerian banks. Customers have to manually set aside money each period and transfer to another account, attracting transaction fees. Most times, users forget to do this or are discouraged because the process of setting money aside is not automatic.

Fintechs such as PiggyVest, Cowrywise etc. are at the forefront of providing convenient processes for regular and periodic savings for Nigerians. Some traditional banks such as Wema (through the ALAT app) and Sterling have introduced automatic savings features through their mobile and online banking applications. These features need to be further refined to enable users to save easily across banks and channels, at little or no cost.

Limited transparency with savings products and services – While some financial institutions in the country try to provide financial education on the savings products and services they provide to customers, there is still a huge simplicity and transparency gap within financial products and services. Sometimes, operating a savings account in Nigeria comes with hidden fees. The average Nigerian that saves does not have enough information about the different savings products from different providers. This makes it difficult to select the best savings product that is tailored to the customer’s needs. Users most times are not clear on what the interest rates are for different savings products. They are also not clear on the terms and conditions that accompany these savings products due to how complex and mystified they sometimes are.

Limited saving products for the poor – There are limited saving products and tools for poor people in Nigeria. The conventional savings products can be expensive to maintain and require access to bank branches or digital devices (smart phones, tablets etc.). Agency banking has been at the forefront of deepening the reach of financial organisations to the bottom of the pyramid, however, there have been limited considerations for innovative products and services that will help the unbanked save money. Saving money for the poor must be accessible (via convenient and available channels), affordable and secure to improve the savings culture of this demographic.

Current issues faced by banks and savings institutions

The absence of seamless interoperability – There is currently a lack of interoperability between the different financial organisations. This makes it difficult for financial systems across multiple organisations to communicate with each other seamlessly. here a customer has a bank account in one bank and wants to save automatically into a bank account in another bank, there’s no seamless way to move the funds directly from a bank account into another bank.

Open banking has the ability to drive effective interoperability across financial institutions.

High operating expenses – A large portion of financial institutions in Nigeria have high operating expenses making it difficult to transfer cost savings to customers. Traditional banks have to maintain physical branches, legacy systems, their employees and still have to spend on front-office processes like KYC, AML and Credit Scoring. With these costs, banks struggle with creating exciting and lucrative savings products that will be attractive to the target customer. Open Banking affords financial institutions the opportunity to outsource aspects of their value chain like front-line office processes to third parties, thereby driving down costs.

Limited access to structured data – While financial institutions have access to customer data, including financial transactions, they do not have a full view of the customers’ financial standing across their assets, liabilities, deposits, investments and transactions across all financial institutions and third parties. This makes it challenging for financial service providers to fully understand customers and provide tailor-made financial advisory services that will help improve a savings culture. For example, it will be counter-intuitive for a bank to advertise a particular savings product to a customer that already has a loan that is being serviced with a lender and takes up a large proportion of the customer’s income but with Open Banking, financial service providers are able to access rich and sufficient information to better understand the customers and their needs.

How Open Banking can solve these issues

Open banking refers to the use of open technologies by financial institutions and third party providers (TPPs) to share data in a standard format to provide more open, transparent and competitive financial services. With Open Banking, customers can give consent to their banks and other financial institutions to share customer data residing on their internal systems with third parties. This data can be used by banks, Fintechs and other savings providers to gain a detailed view of customers’ financial health including information on assets, liabilities, deposits, investments, and transactions across all financial institutions and third parties. This will enable banks and other savings institutions to provide tailored products and services to help Nigerians save, while developing financial knowledge and skills. Open banking can also then create an opportunity for customers to accumulate wealth, by gaining a better understanding of their finances and accessing the best investment products tailored to their financial profile.

Open Banking will contribute to solving the issues that impede adopting and maintaining a true savings culture in Nigeria. Due to open APIs, interoperability between financial systems and organisations will be greatly increased, enabling financial institutions to fully automate the savings process and enable users save money, regardless of the number of accounts they have and want to save money from.

With Open Banking, savings will be more transparent as users will have access to multiple savings products from different providers and be able to choose the one(s) that fits their needs best. This will have a huge impact on the savings culture of Nigerians which will subsequently drive economic growth and financial inclusion.

Why Open Banking is a superior method for solving these problems

- Open Banking makes savings transparent. In addition to fostering innovation, open banking helps to improve healthy competition within the financial services industry. Due to this enhanced healthy competition, financial institutions will have to make their savings products easy to understand by customers and provide detailed information that will support customers in choosing that which is best for them. From one platform, customers will be able to view financial savings products from different providers with simple and clear terms and conditions that apply to each product. This will enable them to assess and select the best one to meet their needs. With the availability of choice, customers can easily switch from one savings provider to another.

- Open Banking improves Personal Finance Management (PFM). Some Nigerian financial institutions currently provide Personal Finance Management (PFM) services to customers, which include savings, budgeting, financial reporting and financial advisory. PFM currently only covers financial data for a particular financial institution providing the service. With open banking, PFM can be more robust, where customers can view a dashboard of their financial health across all their bank accounts, loans etc. This will provide very rich data that will enable customers to understand their financial profile more and choose savings products that are more tailored to their needs.

- Open Banking provides better interoperability across financial service providers. The open APIs leverage the data available across multiple banks to create a single point of contact that unlocks interoperability across multiple financial service providers. This will increase the ease of transferring funds between accounts across multiple financial institutions for the purpose of saving. With better interoperability, Open Banking can also help with cost reduction and efficiencies for Nigerian banks by creating opportunities to outsource parts of their value chain (e.g. AML, KYC, Credit scoring) to third parties in a connected ecosystem.

- Open Banking will ease the savings process and provide customers with better savings experience. Open Banking will solve the issue of cumbersome saving processes and poor user experience currently being faced by users. Due to the fact that providers of these services have gained a better understanding of users, they will be able to provide differentiated savings products and services across their channels. Open Banking will also create opportunities for aggregators to provide multiple savings products from different providers and create platforms that allow users to choose the most innovative and attractive offer. Providers also have the opportunity of providing innovative savings products across channels (such as USSD or through Agents) that will attract the unbanked and enable them to develop a savings culture and create wealth.

- Improved security. Open banking is guided by a standard format of sharing data using open APIs and is largely driven by customer consent. This presents a more secure mode of data interaction as opposed to point-to-point and atypical APIs between financial institutions. Customers are able to gain confidence by seeing that their funds are intact, and adopting Open Banking will also bolster cybersecurity as Nigerian financial institutions and third-party providers will work with standardized and secure API gateways as against custom and proprietary systems that could have hidden vulnerabilities.

- Open Banking is standardized and not proprietary to any single company. One of the benefits of Open Banking is its ability to drive innovation and improve competition within the financial ecosystem. Open Banking will benefit all stakeholders (regulators, banks, customers, fintechs, third parties etc.) and is not a technology or framework that is proprietary to any single company or group of companies. This means that there are endless opportunities that every participant of the savings and investment value chain can leverage.

Saving in the open banking era – Use Case

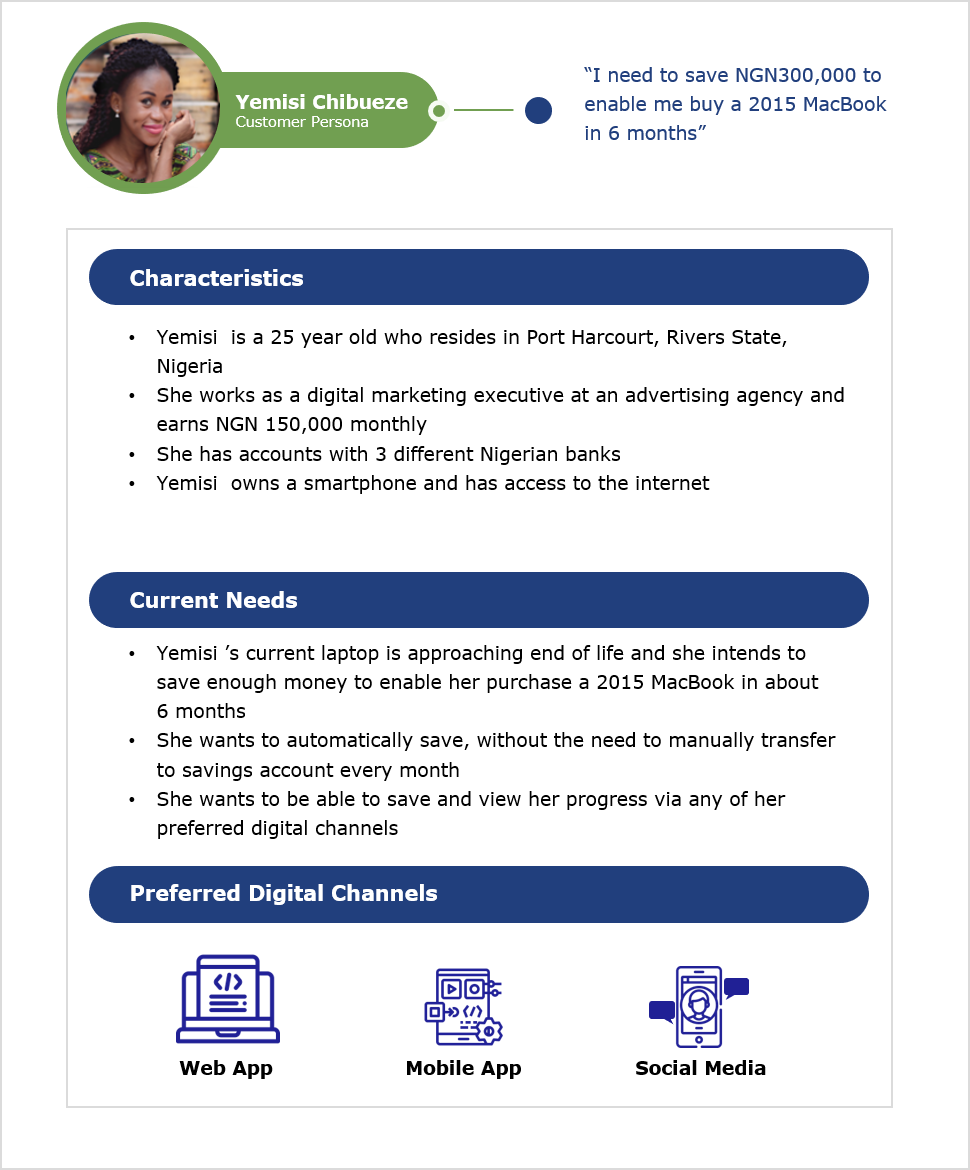

We have developed a use case of how savings can work in the open banking era. A customer persona has been defined to highlight the characteristics and needs of a typical customer.

Figure 1: Illustrative customer persona

From the fictitious customer persona created above, Yemisi Chibueze is a 25-year old digital marketing executive who resides in Port Harcourt, Rivers State and earns NGN 150,000 monthly. She wants to purchase a new laptop from eBay in about 6 months and intends to create a savings plan that will enable her to save that amount automatically and with ease. She currently banks with three Nigerian banks and intends to use a savings application, ‘Pvckette’, to save money (Pvckette is a fictitious app and only exists for the purpose of this use case).

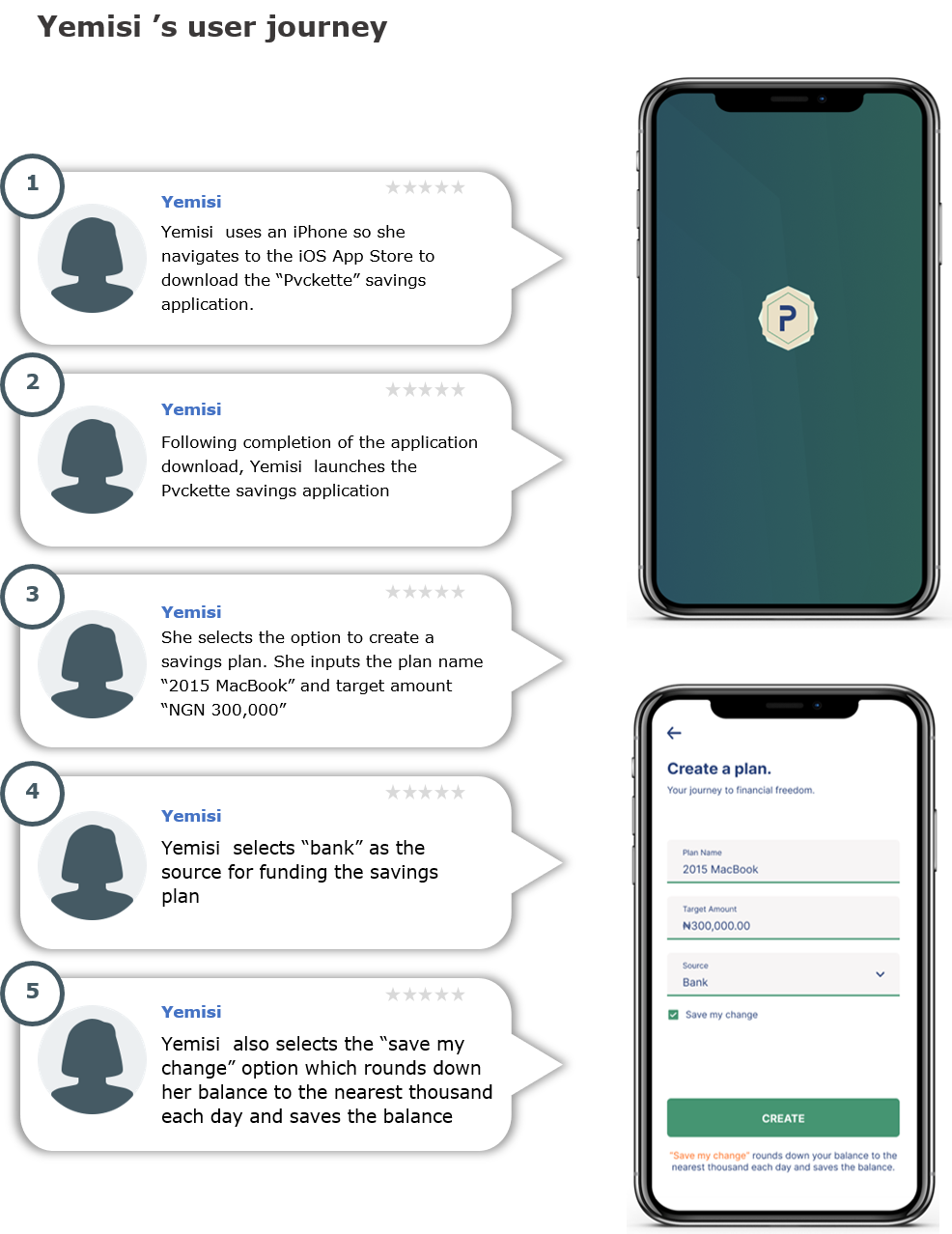

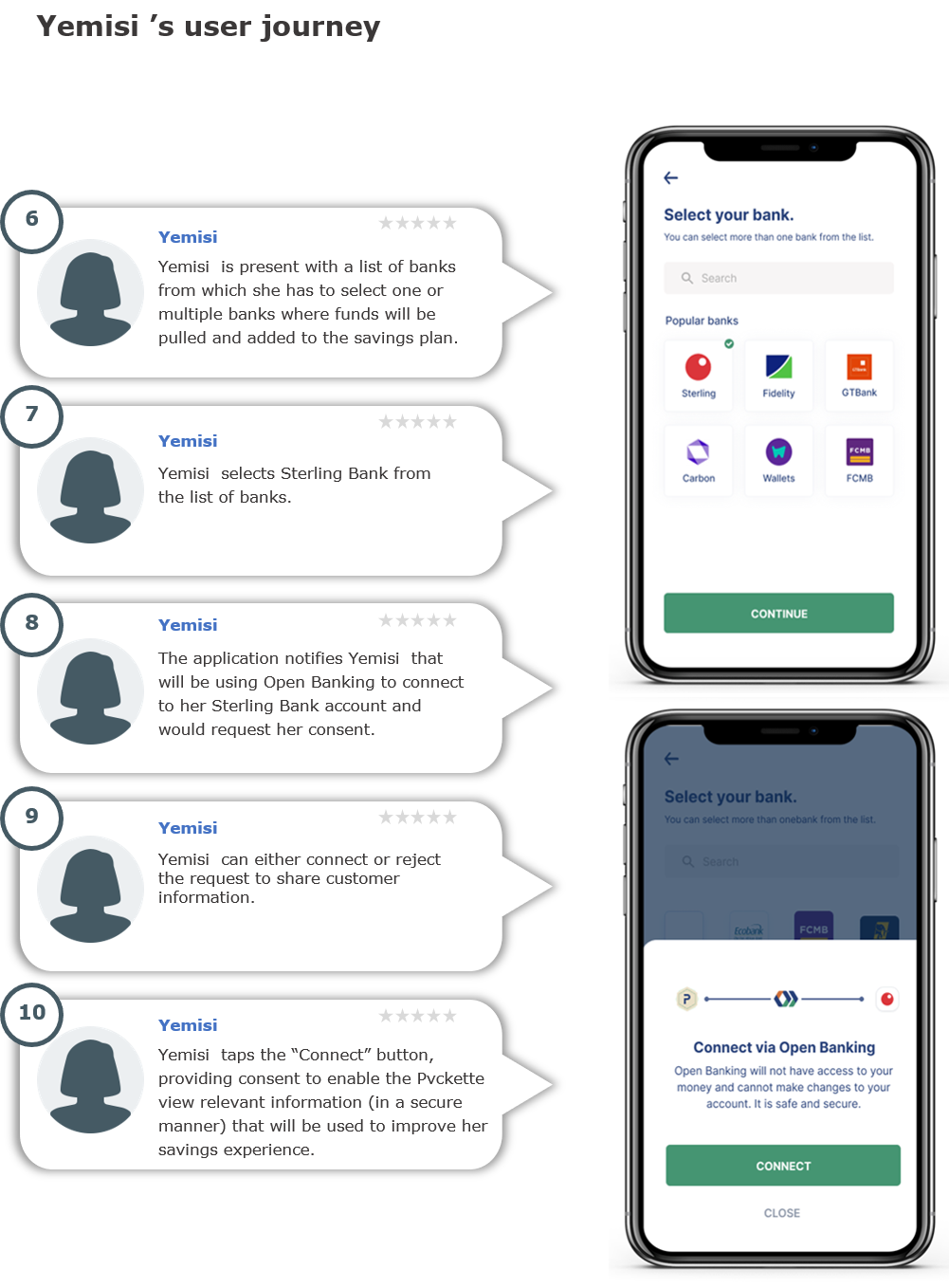

Due to the ease of sharing data in an open model, Yvonne can easily create a savings plan that is tailored to her needs and automatically connect with her bank accounts in a secure manner to fund the savings plan. This increases the convenience and helps to drive a savings culture that will enable her to meet her savings goals.

Yvonne’s user journey

Conclusion

Improving the savings culture of Nigerians will drive financial inclusion and economic growth. Open Banking can be used to transform how Nigerians save money, by reducing the barrier to entry, encouraging the creation of competitive savings products, and making it easier for funds to move seamlessly across financial service providers.

The adoption of Open Banking will catalyze the process by which Nigerians accumulate wealth and prepare for future emergencies

Some of the positive outcomes of this include driving long-term spending abilities and increasing the capital that fuels economic growth. Participants of the Nigerian financial ecosystem (regulators, banks, fintechs etc.) need to explore ways of leveraging Open APIs to provide innovative and inclusive savings products that will improve the life of Nigerians.

References

- Deshpande, R., 2006. Safe and accessible: Bringing poor savers into the formal financial system (No. 38412, pp. 1-16). The World Bank.

- https://data.worldbank.org/indicator/NY.GNS.ICTR.ZS?locations=NG.

- https://nairametrics.com/2020/08/17/breaking-nigerias-inflation-rate-jumps-to-12-82-highest-in-27-months/