Introduction

Banks, Fintechs, and other financial institutions have traditionally relied on internal customer and transactional data as well as credit scores/reports from credit bureaus for credit risk assessment. In developing these credit scores and reports, Nigerian credit bureaus have aggregated and leveraged data from financial institutions to conduct their risk assessment. However, the credit bureaus don’t have access to the majority of data for retail borrowers and conducting credit assessments and checks can be expensive, which makes informal lenders and microfinance banks deliberately avoid using them.

Furthermore, relying on only internal data and credit scores/reports does not give a holistic view as it does not consider the customer’s assets, liabilities, deposits, investments, and transactions across all financial institutions and third parties (Telcos, Energy companies, Retail and lifestyle companies, Insurance, tax authorities, pension companies, etc.). This thus limits the ability to offer personalized lending products and services in real-time. It also restricts the pool of prospective borrowers, as customers with “thin” credit files (limited credit history) are automatically excluded.

Open Banking, which creates an opportunity to “open up” access to customer information through Open Application Programming Interfaces (Open APIs), can help overcome these limitations. Open banking can enable financial institutions and third parties to share data in a standard format to drive open, transparent, innovative, and competitive banking services.

In this report, we explore the lending landscape in Nigeria and rethink how the adoption of Open Banking would impact this.

Lending landscape in Nigeria

The lending ecosystem in Nigeria is made up of different players, including commercial banks, microfinance banks, digital lenders, regulators, payment processors, credit bureaus, lending platform providers, and other service providers (see figure 1 below).

According to Fitch Solutions (formerly Business Monitor International), Nigerian banks provided loans of about NGN 13.6 trillion in 2019, which represented a 6.6% growth from the previous year. This is expected to grow much further due to increasing financial inclusion and regulatory drive for banks to increase and maintain a loan-to-deposit ratio (LDR) of 65% instead of the initial 60%. However, according to National Bureau of Statistics (NBS), 97.43% of loans provided by banks in Nigeria by value are above NGN 10 million, with only 0.77% of loans provided by banks being with the value of below NGN 1 million. This means that most of the loans provided by banks in the country are to SMEs and corporates, with limited retail loans being accessible to MSMEs and individuals.

In addition to credit growth being recorded by banks, there has been a proliferation of Fintechs in Nigeria, providing lending services to customers across digital channels. Lending makes up about 25% of Fintech activity in Nigeria, with digital lenders providing services such as peer-to-peer lending, non-collateral based lending, marketplace lending, etc., to meet customer needs.

Due to the advent of digital technologies coupled with changing customer behaviour, increasing demand for convenience, and fast response to service requests, some Nigerian lenders have been able to transform their lending process, reducing the time-to-serve from weeks or months to minutes, hours and days now. There are currently some banks and digital lenders that disburse loans to customers in minutes of customers completing a loan application. Banks and digital lenders that do this mostly depend on internal data to evaluate the customers, which limits the ability to view the financial health and risk profiles of customers holistically. This keeps interest rates and pricing high as banks, and digital lenders in this category must ensure that the pricing is commensurate with the risk.

It is thus imperative that the entire financial ecosystem reimagines how customers access to credit to ensure that loans are more affordable and accessible, as well as more personalized to each customer’s needs.

What does access to credit in an Open Model look like?

With open banking, banks can leverage open APIs to share customer data residing on their internal systems, securely, with third parties after obtaining customers’ explicit permission. When a customer requests a loan, the lender uses the open banking API to obtain information from all the customer’s relationships across the financial ecosystem, including information on assets, liabilities, deposits, investments, and transactions across all financial institutions and third parties. Subsequently, analytics is conducted on the consolidated information to obtain insights that can be used to evaluate the customers and enhance decision making. The entire process of gathering information and analyzing it is automated and occurs in real-time. The decision of whether to provide the customer with a loan or not can be automated as well, depending on the loan size and the risk appetite of the lender.

How will Open Banking impact the lending landscape in Nigeria?

The adoption of open banking in other markets has led to the increasing array of available information and data sources, enabling lenders and other financial institutions to go much further, generating customer insights that create opportunities to provide better services and cross-selling, while powering product diversification and opening new markets. This would be no different in the Nigerian market. As institutions within the Nigerian financial sector begin to adopt open banking, we expect to see an increasingly transparent ecosystem, where credit is both more available and competitive. We envisage the following impact:

- Open banking will improve the income verification process

One of the key activities of loan origination in Nigeria is the verification of an applicant’s income (individual, SME, or corporate applicant). Lenders request for bank statements from applicants to verify income and assess their transaction history. While some financial institutions are currently able to review these statements and verify income in minutes or hours, and others able to do so in days, open banking can create an opportunity for instant income verification across multiple accounts for the same applicant, in a matter of seconds. Using open APIs that fetch account information and transaction history across the applicant’s accounts with different banks, lenders can automatically categorize transactions and generate insight that can be used to verify income instantly.

- Open banking will help improve the loan collection process

Nigerian financial institutions currently employ several techniques for loan collections (direct debit mandates, automated card debits, customer-initiated payments, etc.). However, there is no full view of the borrower’s account information, and in some cases, customers knowingly default on their loan payments while they move money to other accounts that they know these lenders don’t have access to.

With open banking, the collection process can be transformed, with lenders being able to leverage open APIs to initiate partial or full collections based on the repayment amount agreed for that period, from the borrower’s account with any bank. Open banking-based collections have the potential to reduce delinquency, which can reduce risk premiums and then make loans cheaper, more affordable, and accessible to everyone. More affordable and accessible loans will help improve financial inclusion in Nigeria.

- Open banking will open up new segments of borrowers

Most loan products provided by financial institutions in Nigeria, which are targeted at individuals (personal loans, mortgages, salary advance, credit cards, car loans, etc.) require that the individuals are either in paid employment or can provide collateral to secure the loan. The same applies to SMEs and corporates who will have to show proof of income and sometimes might have to provide collateral to secure the loan. Some of the banks and Fintechs in the country have also provided loan products to individuals without the requirement for the applicant the be in paid employment.

One thing that is common across all the loan products and targets is that the financial institutions that provide these loans require financial and credit information (income information from account statement, credit history, BVN information, etc.) which they use to assess the applicants to determine their affordability and ability to pay back the loans. This has led to a scenario where almost all loans provided by financial institutions in Nigeria are to individuals and corporates with “rich” financial and credit data. In contrast, those with limited financial and credit information are excluded.

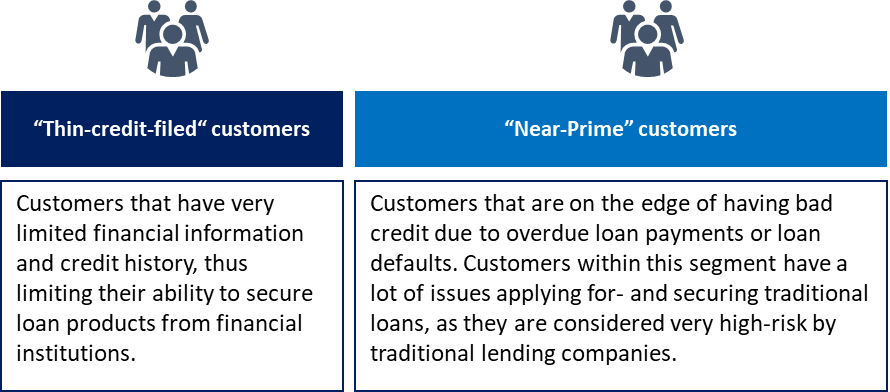

Open banking can open up lending opportunities to excluded segments of customers (“Thin-credit-filed” and “Near-Prime” customer segments). “Thin-credit-filed” customers are those that have the very limited financial information and credit history, thus limiting their ability to secure loan products from financial institutions. With open banking, customers with thin credit files can be assessed and scored using a wide range of information and insight that would typically not be available in a non-open model. Sample information that can be aggregated and assessed includes phone usage and billing history, energy usage history, trends in income and expenditure, etc. An example of an organization targeting this customer segment is Koyo. This UK-based Fintech startup uses open banking to offer loans to people with “thin” credit files and currently poorly served by the market.

Another excluded segment which open banking can help to open up is the “Near-Prime” segment of customers. Near-prime customers are those that are on the edge of having bad credit due to overdue loan payments or loan defaults. Customers within this segment have a lot of issues applying for- and securing traditional loans, as they are considered very high-risk by traditional lending companies. With open banking, this segment of customers can be profiled further to differentiate and ascertain the Near-prime customers that can still repay loans and those that can’t. An example will be an analysis of a near-prime customer’s account data to identify rational reasons for overdue loan payments, which are damaging the customer’s credit score/report. An example of a startup offering loan services to Near-prime customers is Oakam, a UK based Fintech, which takes advantage of open banking to provide loans to consumers with bad or no credit history, and uses data including social networking data, geographic location, and known referrals to make a credit decision.

Fig 3 – Excluded customer segments that can be opened up

Other segments that open banking can help to open up in Nigeria are the informal and MSME segments. Financial institutions can leverage data from relevant third parties to profile and evaluate customers within these segments to evaluate their creditworthiness and provide tailored loan products and services.

- Open banking will help reduce loan defaults and drive responsible lending

Open banking will enable lenders to monitor customers’ financial health holistically. Due to the authorized access to customer account information across the financial ecosystem, lenders will be able to evaluate the financial health of prospective borrowers and easily identify those that will have difficulty in paying back. This will ensure that customers that access personalized loan products can pay back, thus reducing loan default cases and overdue loan payments.

Open banking can also help prevent loan defaults by providing early warning alerts to financial institutions. For example, a continuous and steady fall in account balance over time could signal a decline in the borrower’s financial health and the need to reassess the customer’s credit risk profile. An alert can be triggered for the lender to reach out to the customer to try and understand the reason behind the decline in financial health and how it could impact the customer’s loan repayment plan.

The CBN has issued consumer protection guidelines, which include requirements on “Responsible Lending,” which financial institutions must comply with. One of the pillars of responsible lending is that financial institutions must assess the capability of customers to repay the credit in a sustainable manner taking into consideration the customers’ financial circumstances. This sometimes can be difficult to comply with a non-open model. Leveraging open APIs, lenders can automatically assess the creditworthiness of different segments of customers sustainably while considering their holistic financial health and ability to pay back. Simply put, open banking will directly address concerns around “responsible lending.”

- Open banking will improve competition and drive the creation of innovative loan products

The Nigerian financial ecosystem, if it adopts open banking, will be impacted by competition, which will encourage financial institutions to be innovative in their approach to creating value for customers. This will also have a significant impact on the country’s lending landscape. Open banking has the potential to drive the creation of innovative loan products, different from traditional loans that customers are currently used to. Due to the availability of data, lenders can price loans differently for each customer based on the results of their credit assessment and risk profiling. This can further encourage customers to authorize sharing of their account information with lending service providers, as the more access to data a lender has, the higher the ability to accurately assess the customer’s financial health and provide much lower interest rates based on the customer’s risk profile. In simple terms, customers can get discounts or lower loan rates based on data availability and a lower risk profile.

If customers are not privy to the concept of open banking and the benefits they stand to gain, they will be very averse to sharing their account information with players within the ecosystem, and thus have limited access to innovative loan products which leverage open banking to create higher-value products and services. Hence, financial institutions will be required to create awareness and educate customers on the benefits they can get by granting lenders access to their data.

- Open banking will provide customers with a better experience

Customers have a myriad of reasons why they apply for loan products and want personalization embedded such that they have access to loan products that are tailored to their needs. For example, a customer might want to secure a loan. Instead of equal monthly payments, the customer wants a situation where the monthly interest rate and repayment amount can vary based on the customer’s financial health for that month (e.g., repayment amount can be low in months where the customer has a lot of financial obligations and high in months where the customer has lower financial obligations or receives higher income, e.g., leave allowance, “13th month” etc.).

Open banking can create robust personalization possibilities from lenders and other financial institutions. It gives lenders access to customers’ transactional information, meaning they can go further to understand each borrower on a much deeper level and provide loan products and services that are tailor-made and designed for each specific borrower.

Open banking also has the potential to enable the emergence of loan aggregators. These loan aggregators will typically create a user interface for customers to request for a loan and then, at the back-end, aggregate loan products from different lenders and financial institutions in line with the customer’s request. This then means the customer will be presented with various loan products with different pricing, terms, and conditions, and the customer can choose one that is most tailored to their need (see figure 4 below).

Conclusion

Open banking is completely changing the financial services industry for the better in other markets, and Nigeria looks set to benefit if it adopts open banking. It is clear that access to credit in an Open Banking model is significantly better than accessing traditional loans, which most customers are currently used to. The unlocked data enables faster, more accessible, and more personalized loans available for more people who need it. This will enhance customer experience and help drive financial inclusion across the country.